Archive

Booms, Busts, Stability, Antifragility

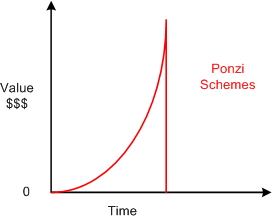

The figure below shows the one time boom-bust pattern of a Ponzi scheme (Bernie Madoff anyone?) We have a meteoric rise in value based on smoke and mirrors where a few get rich, and then an instantaneous dive during which many poor souls lose their shirts. Note that when the bubble pops, the party is over, finished, kaput.

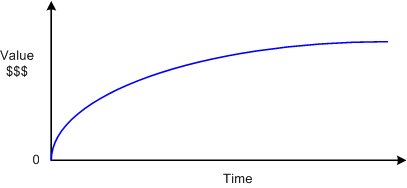

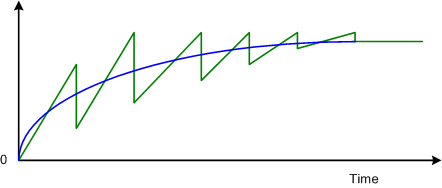

The next figure shows the slow and steady rise in value of a viable, value-creating, system. Since the value the system creates is real, the system achieves stability and remains operational for an enduringly long time. It becomes woven into the fabric of society. At some point, the populace starts taking the system for granted and assumes the system has been influencing their behavior forever.

Here is my sketchy interpretation of what’s happening in the Bitcoin space:

Bitcoin has already experienced several heart-stopping boom-bust cycles throughout its steady march toward stability and widespread acceptance. But note that unlike a Ponzi scheme, which many dooms-mongers (like textbook economists and obsolete, fat-cat, bankstas) loudly claim Bitcoin is after every bust, Bitcoin has not gone kaput. It’s robust, resilient, and dare I say, anti-fragile. The system adapts and get stronger after withstanding every technical and political attack – improving itself via the community driven BIPs process.

Photo credit imgur.com gallery.

Photo credit imgur.com gallery.

The 80-20 Investment Strategy

Instead of following standard Markowitz “portfolio theory“ and allocating your investments across low/medium/high risk financial products according to your age group, Nassim Taleb has suggested that investors adhere to the 80-20 rule: invest 80% of your funds in the most conservative products available (e.g. US treasury bills) and the other 20% in the wildest, riskiest investments that you can find (e.g. startup funding).

Wild and risky investments are those that may go to zero but they also have a small chance of going through the roof. The odds that they go to zero are much greater than the odds of them skyrocketing to Mars.

Mr. Taleb’s thinking is that in a black swan triggered extreme financial crisis (e.g. the crash of 2008), a Markowitz-type portfolio will get demolished across the board. The 80% portion of an 80-20 portfolio susceptible to the black swan will suffer too, but because of its extreme conservative nature the likelihood of massive devastation is much less than for the Markowitz mix. For the remaining 20% segment, the black swan event may actually turn out to be a white swan (e.g. shorting the bull market before the 2008 crash).

I’m too chicken to buck the herd’s “age-based allocation” investment strategy, but I have set aside a small stash of “play money” that I’m willing to lose entirely on a wild and crazy investment.

After a fair amount of grokking, the wild and crazy investment I’ve chosen to risk my play money pool with is….. the fledgling Bitcoin movement.

I am by no means a libertarian ideologue (I lean toward the left), but the Bitcoin movement is fascinating to me for the following reason (plucked from the book “Digital Gold” by Nathaniel Popper):

“The root problem with conventional currency is all the trust that’s required to make it work,” Satoshi (the mysterious, unknown creator of the peer-to-peer Bitcoin network protocol) wrote. “The central bank must be trusted not to debase the currency.” The issue that Satoshi referred to here—currency debasement—was, in fact, a problem with existing monetary systems that had much more potential widespread appeal, especially in the wake of the government-sponsored bank bailouts that had occurred just a few months earlier in the United States. Many believe that the end of the gold standard (by Nixon in the 70s) allowed central banks to print money with no restraint, hurting the long-term value of the dollar and allowing for unbridled government spending.

Another reason why I’m drawn to the bitcoin community is the potential of the system to help the poor – those people who do not have access to bank accounts or credit cards and are forced to deal in cash. The increasing uptake of Bitcoin in Argentina, whose government is notoriousy fiscally irresponsible with its peso currency, is enough evidence for me to believe that the Bitcoin network will do for money what the internet has done for information.

The thing that makes Bitcoin a wild and crazy investment is that….

Bitcoin itself is always one big hack away from total failure.

Since the literal disappearance of 100s of millions of dollars worth of Bitcoins from the Mt. Gox implosion and the high profile “Silk Road” disaster did not kill Bitcoin in the crib, it illustrates the underlying strength and robustness of the system. Thus, I made the first of several Bitcoin buys through the Coinbase exchange:

My strategy is to buy and hold for the long, long term. Oh, and to insulate myself from another Mt. Gox type debacle, I’m moving my Bitcoins off of the Coinbase site and into my own personal Bitcoin wallet as soon as I receive them.

If you want to start grokking Bitcoin for yourself, I suggest looking at the following resources that won me over:

Book: Digital Gold – Nathaniel Popper

EconTalk Podcast: Wences Casares on Bitcoin and Xapo

EconTalk Podcast: Nathaniel Popper on Bitcoin and Digital Gold

The Perfect Person

After listening to two terrific Russ Roberts podcasts on the bitcoin movement, I’ve been grokking the subject for a couple of weeks now. As a result, I created a bitcoin wallet on Xapo.com, which netted me 50 bits worth of bitcoin:

I also started reading “Digital Gold“. The book tells the fascinating story of how the fledgling bitcoin community got started from day one and how it has progressed in fits and starts to where it is today.

While browsing my twitter feed, it somehow dawned on me that Nassim Taleb would be the perfect person to ask about bitcoin. When I did so, all I got was this lousy tee shirt 🙂

Because Of Fools Like You!

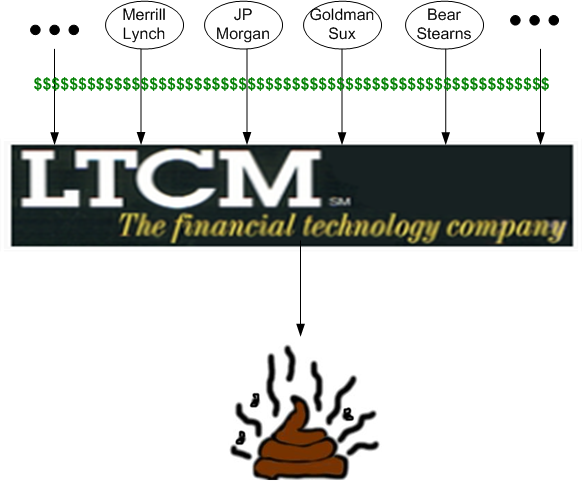

Since Nassim Taleb trashes Nobel prize winning economists Robert Merton and Myron Scholes so often in his books, I decided to look deeper into the disdain he harbors for these two men by reading Roger Lowenstein’s “When Genius Failed: The Rise And Fall Of Long Term Capital Management“.

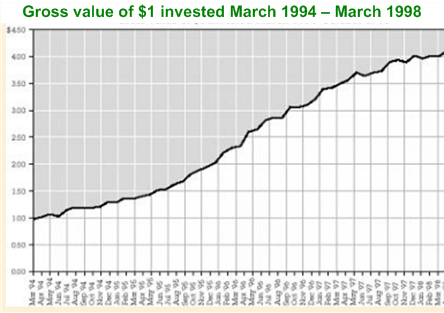

In case you didn’t know, LTCM was a high-falutin’ hedge fund that racked up huge investment gains for four years in 1998 before exploding with a bang that almost shook the financial system to its core. As the following graph shows, if you were privileged enough to have invested $1 in LTCM in March 1994, you would have quadrupled your money by March 1998. Four hundred percent in four years. W00t!

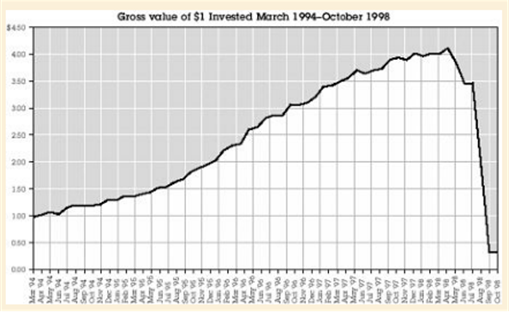

But wait! Looky at how LTCM’s vaunted fund performed between March and October 1998. From $4 to $.25 in eight months. D’oh!

Mssrs. Merton and Scholes were a pair of highly regarded academicians hired by LTCM as the brains behind the mathematically elegant economic models that eventually drove the firm into the gutter. In addition to this dynamic duo, LTCM’s head honcho, John Meriwether, hired several MIT PhDs and a former federal reserve banker to round out his superstar roster. Even before LTCM’s performance began its mercurial ascent, all the big Wall St. banks were tripping over themselves to loan money to, and do business with, the wizards at LTCM.

As you might think, the LTCM partnership thought quite highly of themselves. Thus, they treated everyone else like shit – because they could. They were loaned money at rock bottom prices while charging astronomical fees for their money management “expertise“. Even though LTCM kept their numerous, obscure, huge, derivative-laden trade positions and their precious models secret, the greed of their investors and lenders allowed the elites to do as they pleased.

“There is no way you can make that kind of money in Treasury markets.” Scholes angled forward in his leather-backed chair and said, “You’re the reason—because of fools like you we can.” – Lowenstein, Roger (2001-01-18). When Genius Failed: The Rise and Fall of Long-Term Capital Management (Kindle Locations 693-694). Random House Publishing Group. Kindle Edition.

The LTCM success story began to unravel when Russia defaulted on their national debt in 1998. Since it was “unthinkable” that a nuclear power could ever default on its obligations, the panic quickly spread to other “supposedly uncorrelated” markets around the globe. Of course, the rational Merton/Scholes equations didn’t account for this irrational event. Because of their mammoth size, LTCM couldn’t dump any of their assets like the hysterical herd was doing. Everyone was selling and no one was buying – the market for LTCM’s holdings simply disappeared. LTCM stood by helplessly as their equity tanked faster than you can say WTF! Their fund lost an unprecedented $500M in one day- and they did that twice. Now THAT, takes genius.

Since LTCM was so intertwined with virtually every big player on Wall St., the US Federal Reserve feared that if LTCM went bankrupt the financial system itself could collapse. Thus, the public Fed ended up orchestrating a 3.6 BILLION dollar bailout of the private LTCM by a consortium of Wall St. banks (better them than us taxpayers; but we would come to the rescue in the next panic, 10 years later in 2008). The same people whom LTCM treated like inferior beings had begrudgingly come to the rescue. Even though the LTCM partners were (thankfully) wiped out, the bailers ended up recouping their $3.6B over the next few years. But don’t think of them as heroes. They only signed up for the bailout because they were terrified of sinking too; and their brazen disregard for how LTCM spent their money helped precipitate the meltdown in the first place.

Incredibly, after the bailout, the LTCM fatheads, who were superficially contrite in public, claimed that the panic was a fluke “10 sigma” event. They were (and perhaps still are?) convinced they could mathematically model the human race as a rational-thinking aggregate mass of matter whose “parameters” are dictated by the Gaussian probability density function. A subset of LTCM partners, spearheaded yet again by perpetual loser John Meriwether, started another hedge fund with more complicated models accounting for “fat tail” rare events, but, incredulously, still anchored on the utterly wrong Gaussian distribution. Somehow, they raised $250M from a fresh set of rich idiots.

People caught in such financial cataclysms typically feel singularly unlucky, but financial history is replete with examples of “fat tails”— unusual and extreme price swings that, based on a reading of previous prices , would have seemed implausible. -Lowenstein, Roger (2001-01-18). When Genius Failed: The Rise and Fall of Long-Term Capital Management (Kindle Locations 4176-4178). Random House Publishing Group. Kindle Edition.

As of today, both LTCM and the eggheads’ later fund, JWM Partners, don’t exist – poof!

Pick Your Path

Make a measurement, one measurement, of any personal metric you might fancy… right now. Next, plot your sample point on a graph where time is the independent variable on the x-axis:

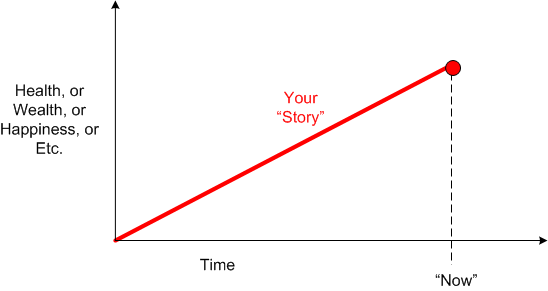

Next, even though you most likely have no prior measurements to plot, reflect on the path that got you to “now“. You’re likely to concoct a smooth, logical, linear narrative like this:

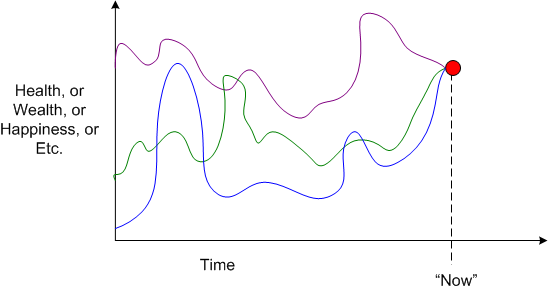

However, because of our propensity to be, as Nassim Taleb says, easily “fooled by randomness“, you’re most likely to have traveled one of the ragged, noisy paths plotted on this graph:

Because of the malady of linear-think, you’re most likely to envision the future as a continued journey on the smooth, forward projection of your made-up narrative. Good luck with that.

A Grain Of Salt

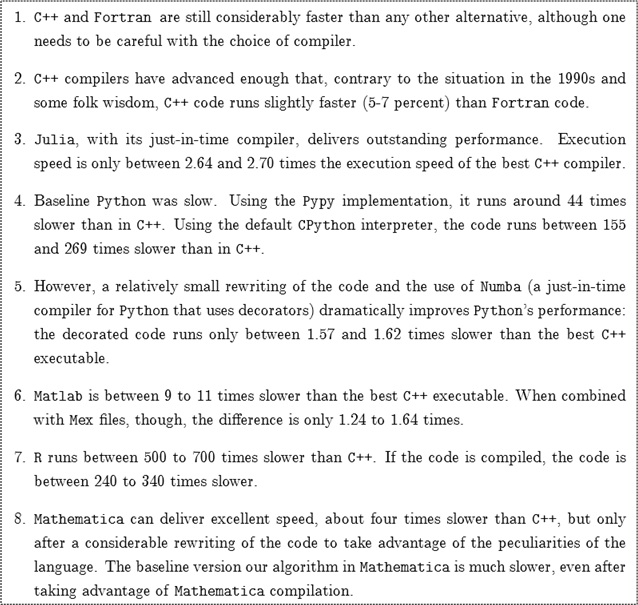

Somehow, I stumbled upon an academic paper that compares programming language performance in the context of computing the results for a well-known, computationally dense, macro-economics problem: “the stochastic neoclassical growth model“. Since the results hoist C++ on top of the other languages, I felt the need to publish the researchers’ findings in this blog post :). As with all benchmarks, take it with a grain of salt because… context is everything.

Qualitative Findings

Quantitative Findings

The irony of this post is that I’m a big fan of Nassim Taleb, whose lofty goal is to destroy the economics profession as we know it. He thinks all the fancy, schmancy mathematical models and metrics used by economists (including famous Nobel laureates) to predict the future are predicated on voodoo science. They cause more harm than good by grossly misrepresenting and underestimating the role of risk in their assumptions and derived equations.

Second Time Around

Since his philosophical ideas are refreshingly new, counter-intuitive, and mind-boggingly deep, I decided to re-read all four of Nassim Taleb’s books. I just finished re-reading “Antifragile” and am now well into my second pass through “The Black Swan“.

As with all good books that resonate with me, I find that re-reading them brings new learning, excitement, and joy. It’s almost like I’m reading them for the first time.

The reason I’m magnetically drawn to Mr. Taleb’s work is because his mission is truly noble and humanitarian. It is to make the world a better place by creating a system in which so-called elites (e.g. economists, politicians, academicians, Harvard-trained managers, high frequency traders) with no “skin in the game” cannot harm millions who follow their predictions/advice/policies without being harmed themselves. Requiring big-wigs to place some “skin in the game” (Mr. Expert, does the content f your portfolio align with your forecasts/advice?) precludes the alarming and increasingly asymmetric transfer of anti-fragility from regular Joe Schmoes like you and me to smug, self-serving elites.

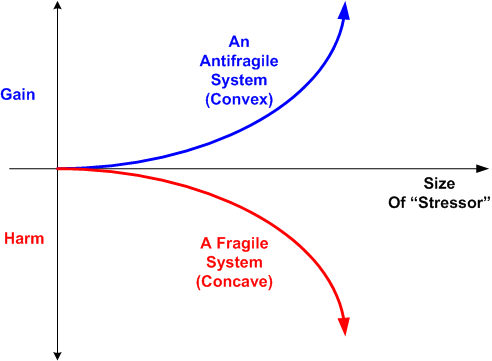

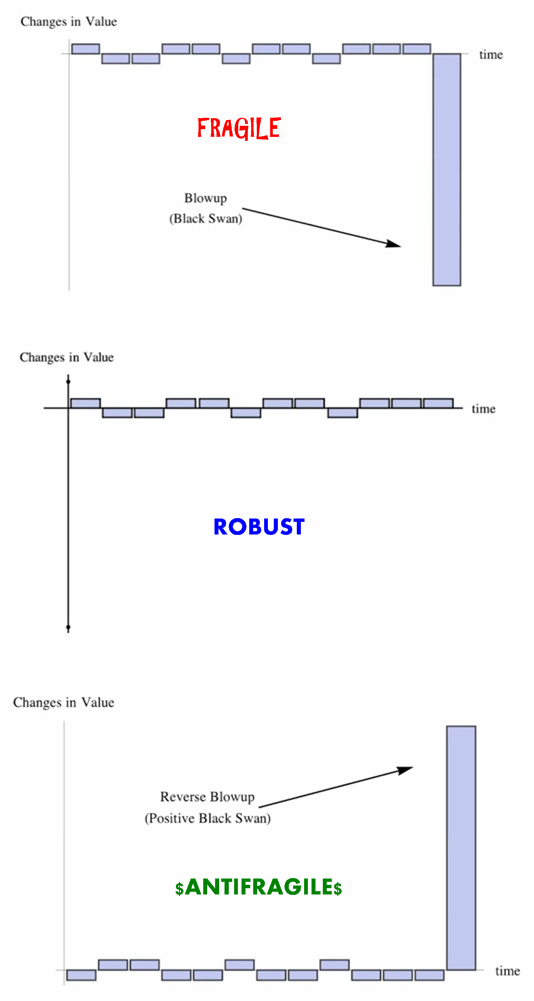

In case you are new to the concept of antifragility, consider the figure below. A fragile system is one in which, as the magnitude of an external stressor is applied, the harm it experiences increases non-linearly. An antifragile system is the exact opposite. It is more than simply resilient or robust. It actually gains from volatility (up to a point, of course).

In case you are new to the concept of antifragility, consider the figure below. A fragile system is one in which, as the magnitude of an external stressor is applied, the harm it experiences increases non-linearly. An antifragile system is the exact opposite. It is more than simply resilient or robust. It actually gains from volatility (up to a point, of course).

Since you can’t know what’s going to happen in the next five minutes, let alone far into the future, you can’t guarantee your own personal antifragility. But you can take concrete action to reduce your fragility and minimize the risk of someone stealing whatever antifragility you do have. Eliminating debt decreases fragility. Adding redundancy (e.g. two kidneys, two lungs) and “having options” reduce fragility. Government bailouts transfer antifragility from taxpayers to executives and shareholders. Lack of term limits transfers antifragility from voters to politicians. Corporate mergers and buyouts transfer antifragility from employees to executives. Increasing size and centralization increases fragility. Lack of exercise increases fragility. Long periods of obsessively manufactured stability increase fragility. The ultimate fragilizer, and the one in which we can only accept, is…….. TIME.

All Upside, No Downside, No Conscience

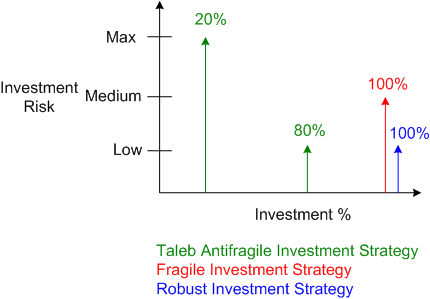

Check out these three financial portfolio performance graphs from Mr. Nassim Taleb:

A fragile portfolio is one which is prone to getting decimated by a rare, unpredictable, event (a.k.a. a Black Swan). A robust portfolio is one which is relatively immune to the effects of a devastating Black Swan. An antifragile portfolio is one which experiences spectacular gains from a Black Swan.

Mr. Taleb asserts that the world’s financial system has been (since the 80’s when we first started bailing out banks), and still is, fragile. As long as bankers know that we, the taxpaying public, will continue to shoulder the cost when they blowup because they are too big too fail, they will continue to exhibit incompetent, reckless, risky behavior backed by bogus PhD calculations. They get their perennial bonuses before each big bust for “doing well“, but aren’t forced to give them back when they lose more money in an instant from a Black Swan than all the profits they’ve ever made previously in the history of banking. It’s a no-brainer with all upside and no downside. What a life… if you don’t have a conscience.

So, how do you construct a anti-fragile portfolio? According to Mr. Taleb, you allocate 80% of your portfolio to “cash” and 20% to wildly speculative investments. It’s called the barbell strategy – weighted investments at both ends of the risk spectrum and nothing in the middle. In the worst case, you’ll lose the full 20%, but the sky is the limit if you’re right with your speculative investment choices. The challenges are:

- To muster up the nerve to actually go against what the mindless “portfolio theory” trained herd says and reallocate your currently fragile portfolio,

- Figure out exactly what Nassim means by “cash” (no, it’s not a savings account at Citibust or Bank Of Nightmerica),

- Decide on which speculative financial instruments to invest in (gold/metals? commodities? real estate? “other”?) .

BD00 knows what these challenges are because, as an unsophisticated investor, he’s struggling to conquer them himself. WTF!

Who Can I Talk To And Where Can I Go?

When I discovered and learned it, I automatically subscribed to the simple but profound principle of POSIWID: the “Purpose Of a System Is What It Does” (not what its stewards say it does). Because of this belief in POSIWID, I’ve always been highly skeptical of supreme experts and people in positions of anointed authority. Almost without fail, and sometimes unconsciously, many of these elites have internally motivated, self-serving agendas while externally offering up their vaunted expertise to “help” you and me. According to POSIWID, their purpose is to serve themselves first, while projecting the appearance of serving others first.

As Daniel Kahneman and other behavioral economics practitioners have discovered, people have an innate tendency to fall prey to the “confirmation bias“. The confirmation bias is where you and I take to heart any and all evidence that we’re “right” on a strongly held belief while ignoring any and all evidence to the contrary. Thus, in order to reinforce my deeply held disdain for supreme experts/authorities, I’ve read all of Nassim Taleb’s books along with these two:

All of the aforementioned books are jam packed full of examples in many domains (medical, financial, political, business, academia) where experts and authorities royally fucked up and negatively impacted the physical and material lives of thousands or millions of people. It wouldn’t be so bad if the perpetrators suffered mightily along with their victims as a result of their own expert bullshit, but it’s galling when they escape unscathed. It’s particularly outrageous when incompetent gurus gain while their constituents lose big.

The most recent egregious example of elites winning big at the expense of the multitude is when Wall St. bankers kept getting bonuses (in order to, uh, retain “talent“) while common people were going bankrupt as a result of their “expert” actions during the 2008 crisis. Even today, six years later, not a single financial big wig was stripped of his/her wealth and/or tossed in jail as a result of his dumbass, irresponsible decisions. Another good example is when an “expert” CEO gets tossed a big golden parachute after being booted out of the company he/she crippled. Applying POSIWID to these types of systems results in:

The purpose of a profit seeking institution is to enrich its elites without regard to the impact of its behavior on the well being of any of its other internal and external stakeholders.

I’d love to explore the flip side of this particular belief, which is the “Purpose Of A System Is What It Says It Does“, but who can I talk to and where can I go to read about it?

Who am I?

Why am I here?

WTF?

Meh!

D'oh!

My BTC Address